Cattle Market Snapshot provided by Northwest Farm Credit Services

January 10, 2014

Cattle markets closed 2013 strong. Key industry drivers include: 1) Improved pasture conditions and lower feed costs: Better moisture conditions in the majority of cattle producing regions significantly improved forage availability. A record large corn crop lowered corn prices and improved feedlot margins. 2) Record high cattle prices: Year over year fed cattle prices increased 8 percent and feeder cattle prices rose 11 percent. 3) Retail beef demand: Retail beef demand was up 3 percent in 2013. Challenges to demand include rising all fresh beef prices, up 4.6 percent during the same period.

Price Discussion

Record prices for all classes of cattle in 2013 are expected to hold into 2014. Recent reports include contract prices for 500 to 550 pound steer calves at $185 per cwt. Exceptions include lower cattle prices in Northern and Central California, where forage is constrained due to drought.

Overall, Cattle Fax’s 2014 outlook projects prices for 550 pound steer calves between $175 to $205 per cwt., prices for 750 pound steers between $150 and $178 per cwt., and prices for fed cattle between $120 and $140 per cwt. Prices for commercial bred cows are also strong, ranging between $1,600 to $2,000 per head.

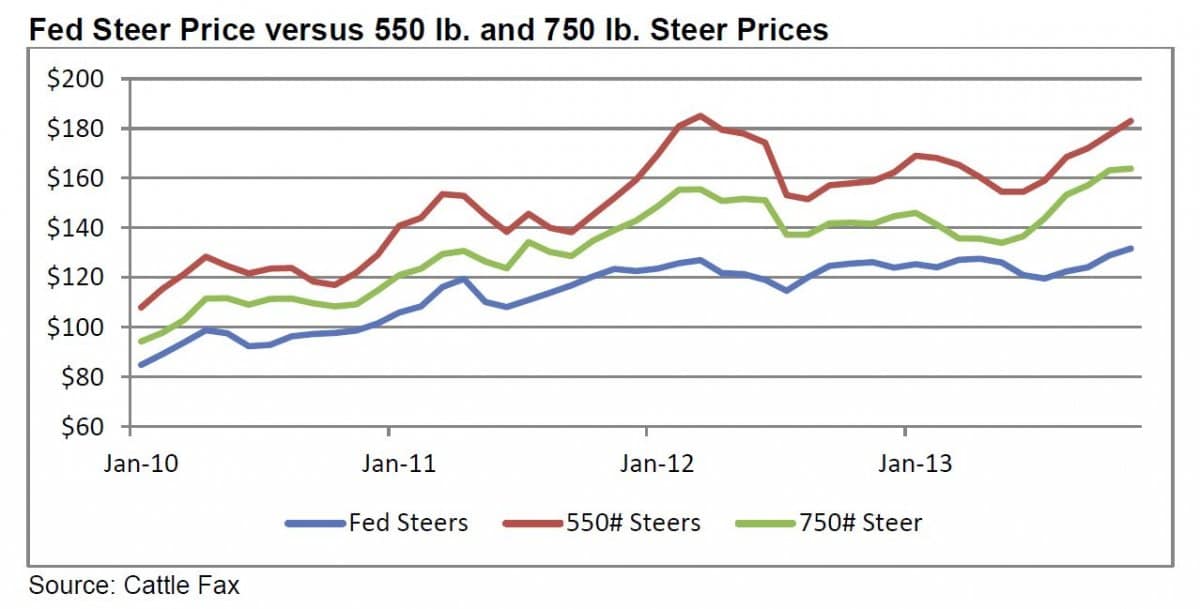

Current prices for 550 pound steers are at a peak last reached in March 2012. Likewise, prices for 750 pound steer and fed cattle are at record levels.

Falling feed prices are the most significant variable supporting feeder cattle prices. Year-over-year corn prices have fallen from near $7 to low- to mid-$4 per bushel.

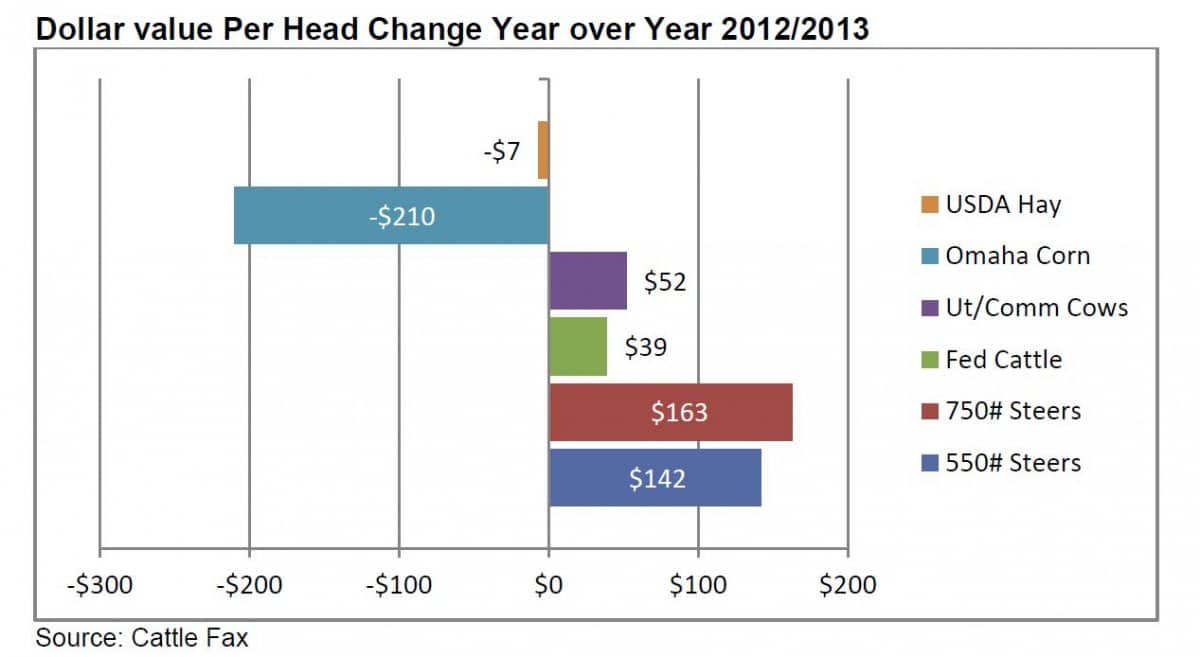

Dollar value Per Head Change Year over Year 2012/2013

Lower feed prices have positively impacted prices for all cattle classes.

Supply and Demand

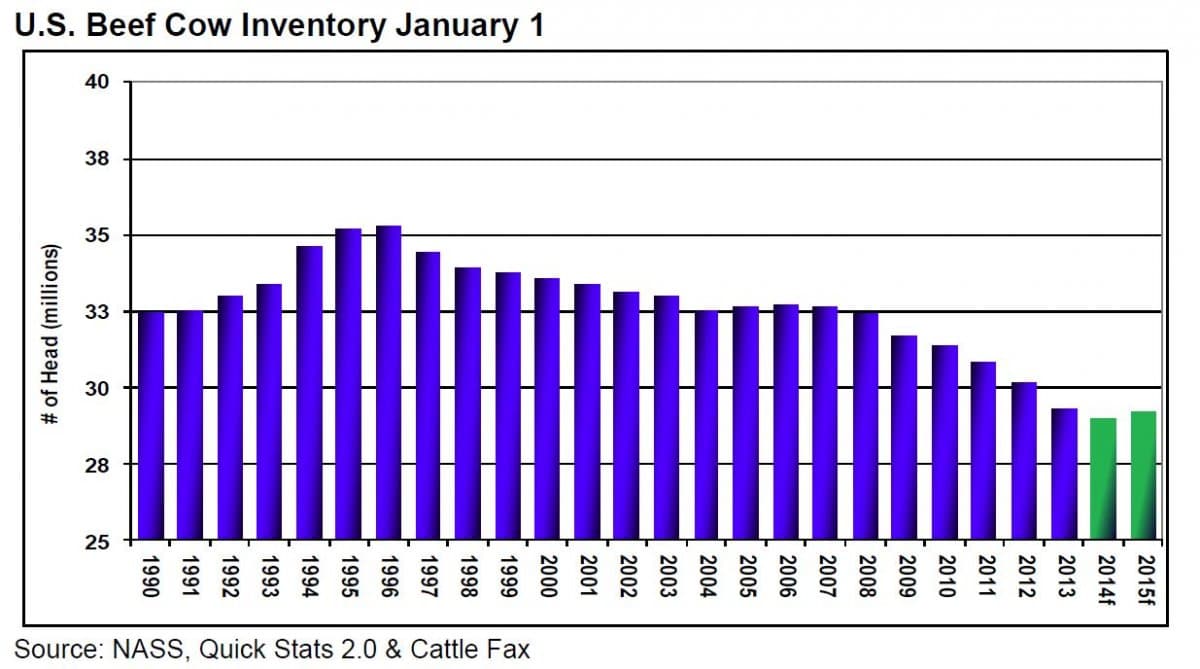

Cattle and beef supplies remain tight. United States cattle numbers are projected down 2 million head

January 1, 2014. However, year over year heifer slaughter as a percentage of all fed cattle slaughter

is down to 35 percent, signaling cow herd stabilization with increased retention of replacement heifers. Cull cow slaughter is also lower, down 3 percent.

U.S. Beef Cow Inventory January 1

Beef cows are forecast down 300,000 head from the prior year as of January 1, 2014.

United States cattle imports from Canada and Mexico in 2013 were mixed. Canadian cattle imports were up 129,000 head, while Mexican cattle imports were down 470,000 head. Cattle exports from the U.S. were up 3 percent in 2013, supported by strong international demand for beef.

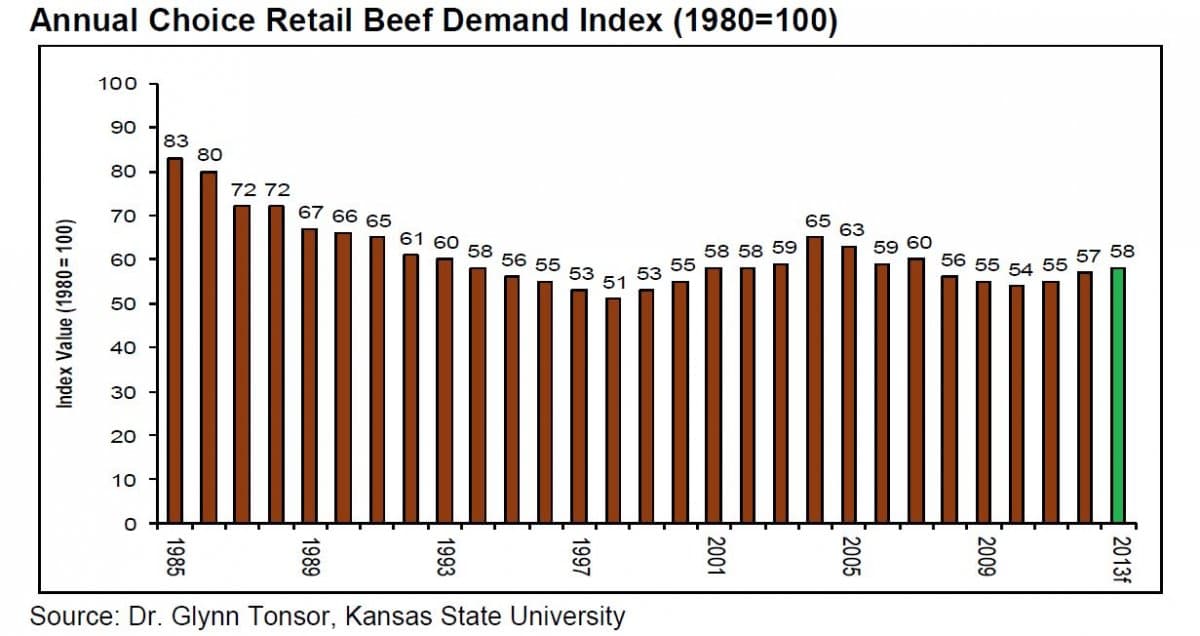

Retail beef prices have increased. Prices for Choice retail beef are up 7 percent, while all fresh beef prices are up 4.6 percent. The Restaurant Performance Index, an indicator of beef demand, improved slowly in 2013, but plateaued in the fourth quarter.

Annual Choice Retail Beef Demand Index (1980=100)

The annual Choice Retail Beef Demand Index rose 3 percent in 2013.

Input Costs

Pasture conditions: Drought conditions have improved dramatically throughout most of U.S. cattle producing areas. The USDA Drought Monitor reports moisture conditions in most of Montana, Northern Idaho and pockets of Central Washington and North Central Oregon as ‘normal.’ Moisture conditions in areas of Southeast Oregon, South Idaho and much of California are reported as ‘severe drought’, with select areas described as ‘extreme drought’ in Southern Idaho and Central California. Above average precipitation is necessary to recharge moisture in drought affected areas to support forage for 2014 grazing. Alternatives for California producers responding to drought include not shipping and feeding hay, placing cattle in feedlots, and/or reducing herd numbers.

Hay: United States hay production has rebounded and prices are 4 percent lower than the prior year. However, local Northwest hay prices may be strong, supported by tight supplies exacerbated by winter conditions. Examples of current Northwest feeder hay prices range between $160 to $200 per ton.

Fuel costs: The U.S. Energy Information Administration expects 2014 gas and diesel prices to decline $0.07 and $0.15 from 2013 averages of $3.50 and $3.92 per gallon respectively.

Interest rates: Short-term interest rates are stable, with the Prime rate unchanged for four years.

Long-term rates have increased slightly, but aren’t expected to increase significantly in 2014.

Northwest land values: Strong commodity prices and low interest rates support stable to increasing Northwest land prices. Northwest pasture rental rates range between $30 to $35 on an animal unit per month basis (AUM). Idaho corn stock pasture rents range between $20 and $40 AUM, with higher rents including full care and supplements. For more information on land values, visit www.northwestfcs.com/resources/land-values.

In the News

- Farmers, ranchers won’t fight antibiotic rule: Farmers and meat-industry representatives share support for the U.S. Food and Drug Administration’s effort to limit antibiotics use in animals raised for meat. Significant changes aren’t expected for U.S. livestock production.

- Tyson adds welfare requirements for beef cattle: Tyson is requiring cattle producers supplying its plants to meet animal welfare requirements in 2014.

- House Farm Bill extension: The House extended the Farm Bill until the end of January as lawmakers work on a new five-year Farm Bill. Separate Senate and House Farm Bills passed in 2013 differ on cuts to food stamps and changes to farm subsidies.

- Country of Origin Labeling (COOL): Tyson no longer accepts Canadian fed cattle at its U.S. slaughter plants due to COOL and other labeling requirements. Long-term impacts to Tyson’s U.S. plants are yet to be determined.

Outlook

A record large 2013 corn crop and improved pasture conditions support strong cattle prices. Expecations are for stable beef cow numbers in 2014 and rising beef cow numbers in 2015. Beef imports in 2014 are projected at levels similar to 2013. Per capita U.S. beef supplies are forecast tight for two to three years.

Beef prices are expected to rise 7 percent in 2014. However, low grain prices will drive larger competing meat supplies, increasing competition for consumers. Key variables in 2014 include U.S. moisture conditions, feed costs, heifer retention, cow slaughter, and calf prices.

![]()

Article Provided by Northwest Farm Credit Services

For more information, please visit www.northwestfcs.com/resources or contact the Knowledge Center by phone at 800-743-2125, ext. 5428 or by email at [email protected].

Disclaimer: This material is for informational purposes only and cannot be relied on to replace your own judgment or that of the professionals you work with in assessing the accuracy or relevance of the information to your own operations. Nothing in this material shall constitute a commitment by Northwest FCS to lend money or extend credit. This information is provided independent of any lending, other financing or insurance transaction. This material is a compilation of outside sources and the various authors’ opinions. Assumptions have been made for modeling purposes. Northwest FCS does not represent that any such assumptions will reflect future events. Past industry trends are not to be considered a guide to future events and actual future events may be materially different from projections. ©Northwest Farm Credit Services 2014