Wheat Market Snapshot provided by Northwest Farm Credit Services

Article written January 10, 2014

Lower grain prices and a shifting marketplace face wheat producers entering 2014. Key factors impacting Northwest wheat growers include: 1) Falling prices: Although U.S. wheat production was down in 2013/14, worldwide wheat stocks rose. Stronger near-term prices are unlikely without a supply disruption. 2) No support from corn: Year over year corn prices have fallen from near $7 to mid-$4 per bushel. Ample supplies of corn are displacing wheat in feed grain channels. 3) Winter weather risks: Temperatures were atypically cold throughout the Northwest in early December. Limited winter kills losses were reported due to snow cover and/or adequate soil moisture. 4) Strong financial position: Northwest wheat producers’ financial positions are bolstered following several years of relatively strong crops matched with solid prices. Strong balance sheets are a solid strategy helping mitigate downside risks related to bearish wheat markets.

Northwest

Extreme cold in early December permeated the Northwest. In Havre, Montana, temperatures dipped as low as -39 degrees. Temperatures eased in Washington, Idaho and Oregon, but remained atypically cold at zero or subzero. Expectations of winter kill are low in most areas. In Montana and Northern Idaho, snow cover mitigated the effects of brutal cold in most areas. Although Washington was absent snow cover, adequate soil moisture should limit losses. However, losses are expected in isolated areas of Northeastern and North Central Oregon, where frigid temperatures and wind met bare winter wheat fields.

Grain prices are dropping alongside temperatures this winter. Generally, futures prices for all wheat classes are +/- 25 percent lower than the prior year. Durum wheat is an exception, down slightly less. Northwest FCS Relationship Managers and regional grain cooperatives report limited new crop sales. Exceptions include areas where grain companies and cooperatives aggressively promoted marketing plans and programs for mitigating downside risks. Anecdotally, producers cite upside opportunities in potential supply disruptions justifying delayed 2014 crop sales.

Wheat producers are expected to end 2013 profitably. Exceptions include select producers in northeastern Oregon where late growing season drought and extreme heat depressed wheat and other crop yields. Current wheat prices are hovering just above most producers’ breakeven of $6 per bushel. Breakeven prices for extremely efficient producers and those with very low overhead may be closer to $5.50 per bushel. Recent years strong prices matched with average to above average yields bolster Northwest wheat producers’ financial position and ability to bear downside risk in 2014.

In wheat industry news, producers are anxious for a final Farm Bill. Key interest areas include questions around crop insurance and determination of Federal premium subsidies. Dry land real estate sales are relatively quiet, with few sales reported during the fourth quarter. Where sales have occurred, prices are strong and in some cases above levels justified by current grain markets. Similarly, anecdotal reports reflect continued optimism and bullish outlooks as producers compete for leases. In most areas, demand for new and used equipment remains strong. However, industry analysts and participants note headwinds suggesting slower equipment sales moving forward, depressed with the expiration of Section 179 of the Internal Revenue Service tax code (allowing first year deductions for equipment purchases up to $500,000) and lower grain prices.

United States and World

Projected U.S. 2013/14 wheat production of 2.13 billion bushels is 6 percent lower than estimated 2012/13 production, but 6.6 percent higher than 2011/12 production. All-wheat estimated harvested acres for 2013/14 fell 3.7 million acres from 2012/13. However, estimated 2013/14 yields of 47.2 bushels per acre are 0.9 bushels higher than 2012/13 yields of 46.3 bushels per acre.

United States production declines are attributed to lower supplies of hard red winter (HRW) and durum wheat. Lower production and imports offset higher beginning HRW beginning stocks. Year over year HRW production fell due to fewer planted and more abandoned acres, and lower yields due to severe drought and spring freeze damage. Conversely, U.S. soft red wheat (SRW) supplies are up, with increases in production and imports offsetting beginning stocks lower than the prior year. Higher SRW supplies are attributed to increases in harvested acres and yields.

Lower U.S. production is partly offset with a 30 percent increase in imports, resulting in projected 2013/14 U.S. wheat supplies of 3.008 billion bushels, 3.9 percent lower than estimated 2012/13 wheat supplies, but 1.1 percent higher than 2011/12 wheat supplies. Higher U.S. imports are largely attributed to record Canadian wheat production and rising exports to the U.S. Canadian growers experienced nearly ideal growing season and harvest weather, leading to yields 21 percent above the historical record.

United States year-over-year projected domestic wheat use is largely unchanged, with the exception of feed and residual use; down 20.1 percent. Large supplies of lower priced corn have displaced wheat used for livestock feeding. However, even at lower levels, feed and residual use remain 91.4 percent above 2011/12 levels.

Exports of U.S. wheat are projected higher for 2013/14 at 1.1 billion bushels, up 9.2 percent from estimated 2012/13 and 4.7 percent higher than 2011/12 exports. However, large wheat supplies in Canada and Australia are expected to increase competition for U.S. wheat exports. Canadian wheat exports are projected to be at their highest since 1991/92. Similar to Canada, 2013/14 Australian wheat production is strong, projected to rise 18 percent over the prior year. At 26.5 MMT, the 2013/14 Australian wheat crop is the third largest on record.

Lower production and slightly higher total use results in projected 2013/14 U.S. wheat ending stocks of 575 million bushels, 20 and 22.6 percent lower than 2012/13 estimated and 2011/12 ending stocks respectively. Specific reductions in U.S. ending wheat stocks include HRW (down 44 percent), SRW (down 28 percent) and white wheat (down 7 percent). Conversely, hard red spring and durum stocks are projected up, 23 and 34 percent respectively. At 23.6 percent, the stocks to use ratio for U.S. wheat is the lowest in five seasons.

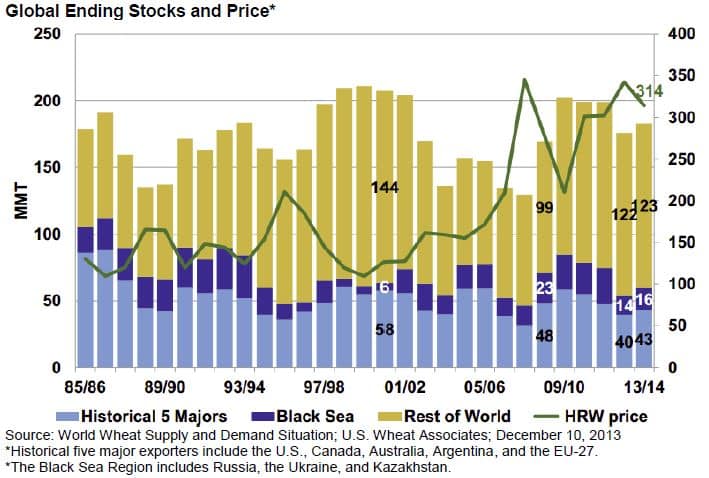

Globally, wheat production is projected at 711.42 million metric tons in 2013/14, 8.4 and 2 percent higher than estimated 2012/13 and 2011/12 production respectively. World wheat supplies in 2013/14 are projected at 1.039 billion metric tons, up 39.1 million tons (3.9 percent) from 2012/13. Exports in 2013/14 are projected at 156.92 million metric tons, up 13.7 percent from 2012/13 and nearly even with 2011/12 exports.

Projected global ending wheat stocks of 182.78 million metric tons are 4 percent higher than 2012/13 estimated ending stocks, but 8.1 percent lower than 2011/12 ending stocks. These stocks represent a 95-day supply of wheat. Projected global ending stocks to use under 26 percent are in line with the prior year and remain the lowest since 2007/08.

Wheat prices are expected to face downward pressure, battling a significant increase in global ending stocks met with only a slight increase in worldwide consumption.

According to U.S. Wheat Associates, 2013/14 production, consumption, trade, stocks and price highlights include:

1. Higher Black Sea, EU and Canadian production, up 34.7, 7 and 38 percent respectively.

2. Record breaking world consumption of 704 MMT, up 4 percent from 2012/13.

3. Rising world wheat exports, up 14 percent from 2012/13, with gains in the Black Sea (up 34 percent), Russia (up 41.6 percent), the U.S. (up 9 percent) and Argentina (up 27 percent).

4. Global ending stocks up 4 percent at 183 MMT, including 31 percent of total global ending stocks in China and the lowest U.S. ending stocks since 2007/08.

Outlook

The USDA projects the 2013/14 season-average wheat price received by farmers between $6.65 and $7.15 per bushel. The 2013/14 season-average price is lower than the 2012/13 record of $7.77 per bushel. Wheat market fundamentals are bearish, pressured by rising global wheat stocks, weak cross market support from corn, and limited worldwide production risks in the near-term.

![]()

Article Provided by Northwest Farm Credit Services

For more information please visit www.northwestfcs.com/resources or contact the Knowledge Center by phone at 800-743-2125, ext. 5428 or by email at [email protected].

Disclaimer: This material is for informational purposes only and cannot be relied on to replace your own judgment or that of the professionals you work with in assessing the accuracy or relevance of the information to your own operations. Nothing in this material shall constitute a commitment by Northwest FCS to lend money or extend credit. This information is provided independent of any lending, other financing or insurance transaction. This material is a compilation of outside sources and the various authors’ opinions. Assumptions have been made for modeling purposes. Northwest FCS does not represent that any such assumptions will reflect future events. Past industry trends are not to be considered a guide to future events and actual future events may be materially different from projections. © Northwest Farm Credit Services 2014